Preliminary Results

Preliminary Results for March 2026

March 2026

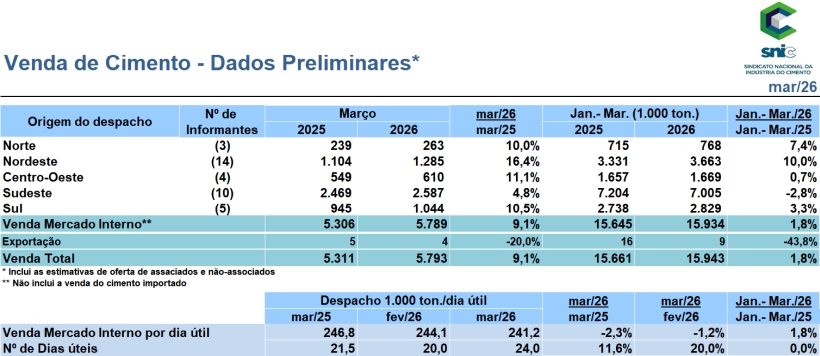

The Brazilian cement industry recorded sales of 15.9 million tons in the first quarter, representing a 1.8% increase compared to the same period last year, according to the National Cement Industry Union (SNIC). In March, sales reached 5.8 million tons, a 9.1% increase compared to the same month in 2025. On a daily basis, sales of the product totaled 241,200 tons, a 1.2% decrease compared to February.

This performance reflects a strong labor market, with the lowest unemployment rate for February in the historical series (5.8%) and 102.1 million people employed, with an average income of R$3,679. These factors strengthened the wage bill and sustained consumer confidence¹, which increased in March.

The positive scenario is further reinforced by the real estate market and the impact of the Minha Casa Minha Vida (MCMV) program, which already accounts for 52% of the volume of new real estate developments in the country. After a 2025 with a 13.5% expansion in launches, the government's goal of reaching 3 million units by 2026 has the potential to generate an increase of approximately 5 million tons in cement demand during the period.

According to data from the João Pinheiro Foundation (FJP) survey released in March by the Ministry of Cities, the resumption of the MCMV (Minha Casa, Minha Vida) program in 2023 helped reduce the Brazilian housing deficit for two consecutive years and closed 2024 at 5.77 million homes, compared to 5.98 million in 2023, reaching its lowest historical level.

In parallel, financing via SBPE (Brazilian Savings and Loan System) signals recovery in financed units, although the sector is cautiously monitoring the Selic rate — which showed a reduction to 14.75% in March. For more than a year, the industry has been monitoring with concern the repeated records of default and indebtedness of the population.

Added to this challenge is the rise of online gambling. According to the TCU (Brazilian Federal Court of Accounts), the expenditure of R$ 3.7 billion by Bolsa Família beneficiaries on "bets" (construction projects) in 2025 signals a diversion of resources that historically were destined for self-construction and small renovations. This factor, coupled with the labor shortage, keeps the construction sector on alert, even though confidence² rose in March, driven by public and private investments in implementation.

In the external scenario, the war between the United States and Iran has generated instability in markets and the global economy, which is directly reflected in international prices of oil, natural gas, and byproducts, impacting the entire production chain.

For the cement industry, this movement brings an additional concern regarding production and logistics costs. Approximately 90% of the raw materials received and the outflow of the finished product are transported by road, and the increase in the price of diesel directly impacts freight.

In addition, there are important repercussions on production costs, such as additives, explosives, and petroleum coke, the main energy fuel for cement manufacturing.

In this context, co-processing presents itself as an important alternative to help diversify the sector's energy matrix, reducing the volatility of energy supply and the carbon footprint. In Brazil, this technology implemented by the cement industry, involving biomass, industrial waste, and Recycled Fuel (RDF), has already achieved approximately 30% thermal substitution, having avoided the emission of approximately 2.8 million tons of CO₂ in the last year.

The Net Zero 2050 Roadmap launched at the last COP30 continues to advance in pillars such as alternative raw materials and fuels, energy efficiency, Nature-based Solutions (NbS), carbon capture and use. At the same time, the sector has been working with the Ministry of Finance, through the Extraordinary Secretariat of the Carbon Market, on the structuring and regulation of the Brazilian Emissions Trading System (SBCE).

“Despite a resilient start to the year, the projection for 2026 is for moderate growth. The sector's performance will depend on internal aspects — such as inflation, interest rates, and economic activity — and external factors, linked to the end of the conflict and the duration of its effects. If, on the one hand, there is an effort to reindustrialize the country with government programs being implemented, on the other hand, there are initiatives such as changes to working hours that, without the necessary technical analysis, are aggravated by occurring in a pre-election period. Furthermore, the regulation of freight price fixing without the necessary technical depth affects the stability, predictability, and resumption of growth in Brazilian industry.” Paulo Camillo Penna – President of SNIC