Preliminary Results

Preliminary Results for January 2026

January 2026

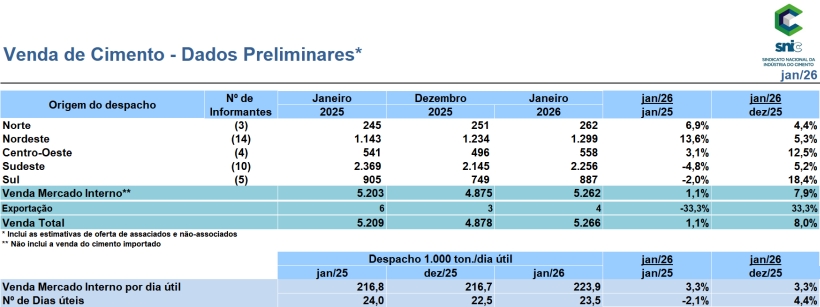

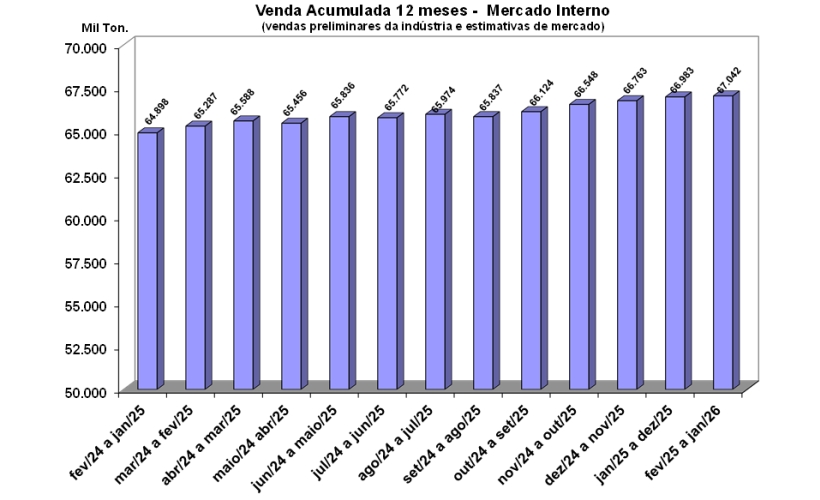

The cement industry recorded a favorable start to the year in terms of sales performance, with sales of the input in the country totaling 5.3 million tons in January, a growth of 1.1% compared to the same month of 2025 and an increase of 8% compared to last December. On a working day, sales totaled 223,900 tons in the month, representing an increase of 3.3% compared to the same month of the previous year. It is worth noting that consumption was impacted by the volume of rain in the South and Southeast regions.

Even so, the warming of the labor market and the increase in the population's income remain pillars of consumption. The unemployment rate ended the year down, reaching 5.1% — the lowest level since 2012 — and the employed population hit a record of 103 million people. With average income at R$ 3,560 (higher than R$ 3,368 in 2024), the wage bill reached historical levels, while formal employment reached 38.9 million jobs, reducing informality to 38.1%.

In this scenario, construction confidence¹ rose to its highest level since March 2025, driven by infrastructure investments, record hiring under the Minha Casa, Minha Vida (MCMV) program, and new financing rules for middle and high-income earners. In the accumulated total for 2025, MCMV sales grew by 15.5%, consolidating the program as a key component of the sector. The industry² also began January recovering optimism after a pessimistic year-end, showing improvement in demand and inventory flow.

However, the sector faces challenges such as maintaining the Selic rate at 15% per year and the high indebtedness of families, which reached 49.77% in November. Consumer confidence fell in January after four consecutive increases, reflecting the weight of interest rates and default rates, which already affect 81.2 million Brazilians. In addition, the shortage of labor in construction remains a structural bottleneck for 2026.

Despite external uncertainties and restrictive monetary policy, the outlook for the year remains resilient. Inflation is on a downward trajectory and there are signs of a reduction in the Selic rate to 12.25% by December. In terms of sustainability, the sector remains focused on the regulation of the carbon market, the consolidation of the Brazilian Emissions Trading System (SBCE), and the decarbonization targets of the Climate Plan, in which the sector has an effective participation.

“We started 2026 with the construction industry's confidence at its best point in the last ten months. The resilient job market and rising incomes form a solid base, but we still face the challenge of interest rates at 15%, which penalize medium and high-end mortgage lending and household consumption. Our expectation rests on the start of the Selic rate cut cycle scheduled for March and the continuation of investments in infrastructure and the Minha Casa, Minha Vida program, which remain major drivers of cement consumption in the country. Inflation converging towards the target and a more stable exchange rate could also become important allies for the sector in the coming months." Paulo Camillo Penna – President of SNIC