Preliminary Results

Preliminary Results for December 2025

December 2025

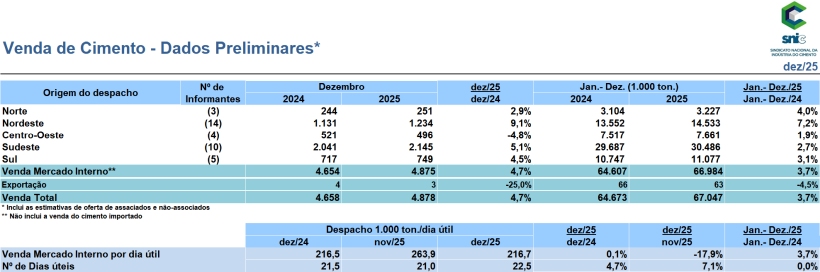

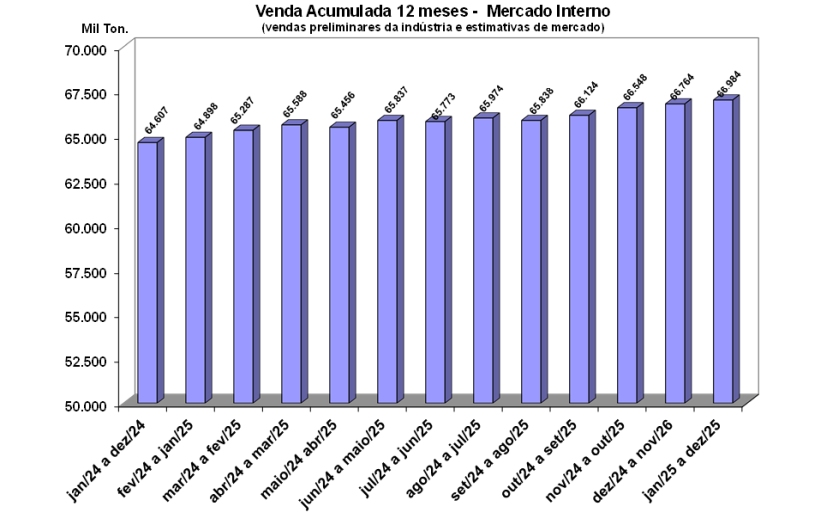

Cement sales in December totaled 4.9 million tons, a 4.7% increase compared to the same month in 2024, according to the National Cement Industry Union (SNIC). With this result, the sector ended 2025 with a total of 67 million tons sold, accumulating a 3.7% increase in 2025 — which represents 2.4 million tons more than the previous year.

The activity consolidated the recovery that began with the 3.9% recovery recorded in 2024. The performance corroborates the expansion trajectory, although the total volume is still far from the historical record of 2014, of 73 million tons.

All regions showed accumulated annual growth, led by the Northeast (7.2%), followed by the North (4.0%), South (3.1%), Southeast (2.7%) and Midwest (1.9%).

2025 was marked by a macroeconomic scenario of contrasts. On one hand, the sector was boosted by the heating up of the labor market: unemployment¹ fell to 5.2% in November — the lowest in the historical series, with 5.6 million unemployed people — while the employed population reached a record 103 million and average income registered the highest value ever recorded, expanding the wage bill, which has a strong correlation with the sector's sales.

On the other hand, the economy faced a slowdown in GDP throughout the year and a contractionary monetary policy. The Selic rate reached 15% in June and remained at this level throughout 2025, the highest level since July 2006. This situation reduced mortgage lending via savings (SBPE). The situation was aggravated by high indebtedness (compromising 49.1% of the population's income) and record defaults², which reached 80.4 million people in October, the highest in the series. In addition, there was strong competition for the family budget with electronic betting. In the housing construction sector, the Minha Casa, Minha Vida (MCMV) program has established itself as an essential driver for the cement industry. In the year to September, program launches grew by 7.9%, while sales registered a 15.5% increase. The North region stood out, where the program accounted for 60% of real estate launches. The Southeast region had the highest number of units launched, with 34,099 properties in the third quarter.

The expansion to new income brackets and the new credit rules — which will increase funding to up to 100% of savings and a higher ceiling on property value — combined with changes in Income Tax, seek to restore the purchasing power of the middle class and reduce the housing deficit.

In infrastructure, sanitation continued to attract investments. In the road segment, concrete pavement continued to advance as a more durable, sustainable solution aligned with the decarbonization guidelines of the Ministry of Transport. States like Paraná, Santa Catarina, Goiás, and the Federal District have stood out for their strong investments in this technology. The solution has also been replicated on streets and avenues in about 200 municipalities, enhancing attributes such as reduced fuel consumption, heat islands, and increased street lighting.

This progress goes hand in hand with climate responsibility. Brazil maintains one of the lowest carbon intensities in the world (580 kg CO₂/t) and has accelerated its energy transition: co-processing – energy generation from alternative fuels – has reached 30% of the energy matrix, equivalent to 3 million tons of waste and biomass, avoiding the emission of 2.8 million tons of CO₂.

Raising climate ambition, the sector launched the Net Zero Roadmap at COP30. Through it, SNIC mapped a series of levers, within the production process and throughout the product life cycle, to achieve emissions neutrality by 2050. These are measures that include greater use of alternative additives and raw materials, expansion of alternative fuels to replace non-renewable fossil fuels, greater efficiency in the production of concrete and construction systems, use of clean energy, carbon capture and storage, and nature-based solutions.

In addition, the activity was integrated into Mission 5 of the New Industry Brazil (NIB), being recognized as strategic for industrial decarbonization, and was at the forefront of the debates on the Climate Plan, approved by the government in December 2025.

In innovation, hubIC3 — a partnership with USP, ABCP and SNIC — continues to drive digital construction towards Industry 4.0, with emphasis on the coordination of the More Network, a pioneering project to measure the CO₂ footprint of housing, aiming to promote the low-carbon economy.

This convergence between tradition and innovation paves the way for 2026, a year of double celebration: the beginning of the journey towards the 90th anniversary of the Brazilian Portland Cement Association (ABCP) and the centenary of the Brazilian cement industry. The sector, present in 23 states, recorded revenues of around R$27 billion and generated 85,000 jobs direct and indirect costs and maintains the investment forecast of R$27.5 billion between 2023 and 2027.

“The performance of the Brazilian cement industry in 2025 was in line with SNIC's projections, supported by the Minha Casa, Minha Vida program and the advancement in infrastructure, strengthening concrete pavement as a strategic and sustainable solution. We also celebrate the success of our environmental agenda, with a record in co-processing and the launch of the Net Zero Roadmap during COP 30. We closed the year consolidating the recovery, but attentive to the economic situation, especially the Selic rate and the impact of indebtedness on family income.” Paulo Camillo Penna – President of SNIC

Perspectives

The economic scenario marked by fiscal uncertainties of the government, with the Selic rate at high levels, coupled with high indebtedness and default of the population indicates that the growth rate of cement consumption will be moderate in 2026.

However, three important vectors may sustain consumption during the year.

Housing: The government's new goal of contracting 3 million housing units under the Minha Casa, Minha Vida program by 2026, 1 million more homes than the previous target, could generate an increase in cement consumption of around 5 million tons. Solutions such as cast-in-place concrete walls and concrete blocks will be crucial to making this volume viable quickly and at a lower cost. The impact on the sector is direct: a 45 m² housing unit consumes 6 tons of cement if built with concrete walls, or 4 tons if concrete blocks are used.

Transportation infrastructure: Brazil has only 13% of its road kilometers paved and, therefore, a great opportunity to use rigid concrete pavement on these highways. This is an economical and highly durable solution, which minimizes maintenance costs. In addition to being sustainable, it optimizes fuel consumption and tire life, mitigates heat islands, and increases road visibility. All this using cement, an input that is increasingly aligned with emission reduction targets. With only 57% of existing roads in fair or poor condition, there is a vast field for restoration work via whitetopping (concrete resurfacing over asphalt). The Ministry of Transport's new guidelines for allocating resources in highway concession contracts, aimed at mitigating greenhouse gas emissions, directly favor rigid pavement, which consumes approximately 939 tons of cement per kilometer restored.

Basic sanitation: In 2026, the sector will continue to be heated with large auctions, attracting investments from private concessionaires, driven by the new legal framework and the pursuit of universal access, focusing on structural works that could generate demand for cement.

Therefore, SNIC projections indicate an expansion in cement demand in 2026, provided that programs emphasizing housing, sanitation, and logistics are implemented.