Preliminary Results

Preliminary Results for November 2025

November 2025

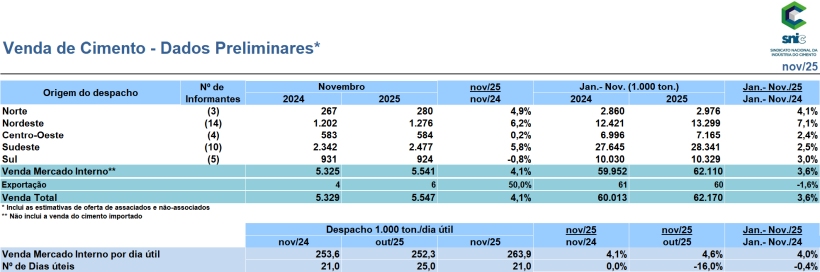

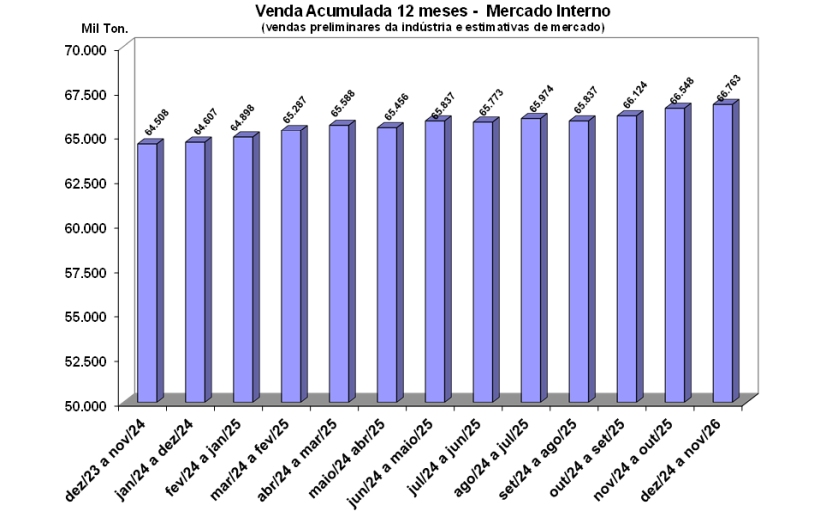

Cement sales in November totaled 5.5 million tons, representing a 4.1% increase compared to the same month in 2024, according to the National Cement Industry Union (SNIC). In the accumulated year (January to November), the numbers reached 62.2 million tons, a growth of 3.6% compared to the same period last year. Cement shipments per working day reached 263,900 tons.

The sector's performance continues to be influenced by a highly complex macroeconomic scenario. On the one hand, data show robustness in employment and income: unemployment reached 5.4% in October, the lowest in the historical series, with only 5.9 million unemployed people. The employed population registered a new record (102.5 million) and average income reached the highest historical value, boosting the wage bill. The heated labor market increased consumer confidence in November, reaching the highest level since December 2024¹.

On the other hand, in addition to the GDP slowdown throughout the year, the credit and consumption environment remains challenging. Inflation expectations for 2025 and 2026 remain above target, pointing to the need to maintain high interest rates. This monetary tightening is directly reflected in the population's indebtedness, which grew to 49.1% in September, and in defaults, which reached a record 80.4 million individuals in October. Additionally, spending on bets continues to put pressure on family budgets.

The scenario of uncertainty, driven by the contractionary monetary policy, impacted industry confidence², which fell for the eighth time this year due to weak demand and high inventories. In construction³, although confidence rose in November driven by the infrastructure and specialized services segments, the level is still insufficient to recover the level at the beginning of the year.

In the construction materials retail sector, sales fell 2% in October compared to the previous year, leading the sector⁴ to reduce, for the second time, its 2025 growth projection from 1.8% to 0.5%.

The real estate market shows mixed signals. While launches rose 1.6% in the 3rd quarter, sales fell 6.5% in the same period, increasing the volume of units in stock. Real estate financing via SBPE suffered a sharp contraction, with a 36.12% drop in the number of units financed for construction in the accumulated period up to October, reflecting the rise in interest rates.

However, the Minha Casa, Minha Vida (MCMV) program continues to be a crucial driver of demand. In the accumulated period of the year, launches under the program grew 7.9% and sales increased 15.5%. The impact of MCMV on the cement industry is significant: a 45 m² unit consumes between 4 and 6 tons of the input, depending on whether it is built with concrete blocks or walls. The sector projects that to reach the goal of exceeding 2 million units between 2023 and 2026, cement consumption will be considerably expanded.

In addition to this, there are new housing credit rules, which will allow the use of up to 100% of savings resources and raise the financing ceiling, measures that, combined with changes in Income Tax, seek to restore the purchasing and investment capacity of the middle class and reduce the housing deficit even considering current interest rate levels.

In parallel with market prospects, the country's cement sector reinforces its global commitment to decarbonization. In November, the industry presented its new Net Zero 2050 Roadmap during COP30 in Belém, detailing the route to carbon neutrality supported by a solid sustainability trajectory. Brazil already stands out on the world stage, emitting 580 kg of CO₂ per ton of cement, a figure lower than the global average of 610 kg/t. Furthermore, the sector has consolidated itself as a benchmark in the replacement of fossil fuels, reaching 32% of its energy matrix from alternative fuels, such as biomass and waste, reaffirming co-processing as a crucial activity in the energy transition.

“The cement industry is approaching the end of 2025 closely observing the dynamics between the heating up of the labor market and the constraints on credit. While the real estate market financed by savings suffers from high interest rates, social housing confirms its strategic role. The progress of the Minha Casa, Minha Vida (My House, My Life) program and the continuous investments in infrastructure, with emphasis on the strong expansion of road and urban concrete pavement, combined with our renewed commitment to the climate agenda, will be decisive in sustaining demand next year” Paulo Camillo Penna, President of SNIC.